New FTC Rule Will Make it Easier to Cancel Subscriptions

Last updated October 17, 2024

UPDATE: On July 8, 2025, the U.S. Court of Appeals in St. Louis blocked enforcement of the FTC’s Click-to-Cancel rule. The court decided the commission had not followed proper procedure, as alleged by several business groups—an assertion the commission rejected. Checkbook’s original story follows. Click here to read our updated story.

Listen to audio highlights of the story below:

Wouldn’t it be nice if every company made it as easy to cancel a subscription as it was to sign up? Of course, many don’t. It’s frustrating to call customer service lines that aren’t answered or get lost in phone tree “doom loops” that never let you talk to someone. Why is there a big button to “subscribe,” but it takes click after click to find the small print that explains how to cancel? Or why could you sign up online, but are required to mail a certified letter to cancel?

“I think almost everybody I’ve talked to has a story about trying to cancel a product and how difficult it was,” said Erin Witte, director of consumer protection at the Consumer Federation of America. “And this is not by accident; this is by design.”

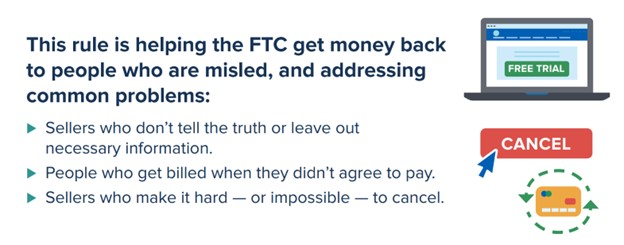

The Federal Trade Commission (FTC) wants to end these unfair and deceptive practices and give consumers greater control over their subscriptions. On Oct. 16, the commission approved the final version of a new “Click to Cancel” rule that requires businesses to make their cancellation processes “at least as easy to use” as their sign-up methods.

(The FTC’s Click to Cancel rule passed by a vote of 3 to 2, with both Republican commissioners voting against it.)

“Too often, businesses make people jump through endless hoops just to cancel a subscription, said FTC Chair Lina Khan. “The FTC’s rule will end these trips and traps, saving Americans time and money. Nobody should be stuck paying for a service they no longer want.”

Subscription programs have grown in popularity in recent years, as companies look for ways to retain customers and boost revenue. These programs can provide substantial benefits, such as free shipping, discounted prices, or special offers.

But when someone wants to cancel, they should be able to do it “quickly and easily,” the FTC said. And that process should be offered through the same medium (online, phone, etc.) people used to sign up.

When it takes full effect next year, the new rule should help eliminate the frequent hassles involved with ending unwanted subscriptions for everything from streaming services and gym memberships to automatic shipments of cosmetics and nutritional supplements.

“This is going to save people a lot of time, a lot of money, and it’s going to ensure that they get the products and the subscriptions that they really want, not just what they felt like they forgot about, or they relented because they couldn’t figure out the cancellation process,” Witte told Checkbook.

Click below to listen to our Consumerpedia podcast episode on "dark patterns."

In its news release on the new rule, the FTC warned businesses that their cancellation processes should not be overly burdensome. And it provided three guardrails for them to follow:

- You can’t require people to talk to a live or virtual representative to cancel if they didn’t have to do that to sign up.

- If you offer cancellation by phone, you can’t charge extra for that service, and you must answer the phone or take a message during normal business hours. If you accept messages, you must respond promptly.

- If people originally signed up for your program in person, you can offer them the opportunity to cancel in person if they want to, but you can’t require it. Instead, you need to offer a way for people to cancel online or on the phone.

Complaints Skyrocket About Negative Option Marketing

The Click to Cancel rule is part of the FTC’s ongoing review of its 1973 Negative Option Rule, which regulates unfair or deceptive practices related to subscriptions, memberships, and other recurring-payment programs.

“Negative option marketing” is an old business practice that is often confusing and costly to consumers. It’s when a seller interprets a customer’s failure to take affirmative action to reject an offer or cancel an agreement as permission to be charged for goods or services. Negative option marketing includes subscription services that automatically renew unless the customer affirmatively cancels, and free trial offers that convert to paid subscriptions unless canceled within a limited time period.

All too often, merchants don’t adequately disclose all terms and conditions, bill people without their consent, or make cancellation difficult or impossible. Companies that follow best practices contact customers prior to the subscription renewal to give them adequate time to cancel.

The FTC receives thousands of complaints annually about negative option marketing and recurring subscription practices. The number of complaints has been steadily increasing over the past five years, the commission said. In 2024, it received nearly 70 consumer complaints per day on average, up from 42 per day in 2021.

“Free trial” offers are especially problematic. In most cases, if you don’t cancel on time, you’ll be charged for that “free” product or service. You could also be automatically enrolled in an ongoing subscription program. Many customers don’t understand this, because that information is not disclosed or hidden in fine print.

Cancelling that subscription can be difficult at best; impossible if you’ve fallen for a free-trial scam. Because the company has your credit or debit card number, which you provided to cover shipping and handling, they can continue billing you.

Checkbook tip: It’s best to pay for any subscriptions that bill automatically with a credit card. If you cancel and the company continues to bill for services you don’t want, you can challenge those charges with your credit card company. It might be more difficult to get reimbursed for recurring fees charged to a debit card.

The commission’s updated Negative Option Rule will:

- Prohibit sellers from misrepresenting any material facts when using negative option marketing.

- Require sellers to “clearly and conspicuously” disclose important terms of the offer before obtaining a consumer’s billing information.

- Require sellers to obtain the consumer’s “informed consent” to the negative option features before charging them.

“The FTC’s new rule is an important recognition of the struggles consumers have been facing to free themselves from hidden contract language and misleading practices,” said Shennan Kavanagh, director of litigation at the non-profit National Consumer Law Center.

The provisions “are really common sense,” she told Checkbook. “[They] will make sure that consumers are not unwittingly having money taken straight out of their bank accounts for services or products that they no longer wish to use.”

More from Checkbook:

Consumerpedia podcast, episode 36: Dark Patterns: Sales Tactics Designed to Deceive

More from the FTC:

- Getting In and Out of Free Trials, Auto-Renewals, and Negative Option Subscriptions

- FTC Report Shows Rise in Sophisticated Dark Patterns Designed to Trick and Trap Consumers

Contributing editor Herb Weisbaum (“The ConsumerMan”) is an Emmy award-winning broadcaster and one of America's top consumer experts. He has been protecting consumers for more than 40 years, having covered the consumer beat for CBS News, The Today Show, and NBCNews.com. You can also find him on Facebook, Twitter, and at ConsumerMan.com.